I noticed the below charts of certain Salvage Materials moving up off the dials recently (all charts are over a year):

Now, this is not the case for all Salvage Material items - hence i don't think this indicates a lack of supply (or activity from salvage) as a general theme though this perhaps plays a part.

. . . . . clearly, these are Citadel related materials where demand is noticeably outstripping supply.

Furthermore, i am thinking that the current war is diverting activity away from salvaging activity - hence, supply is perhaps unable to react in the short term.

I have not checked but i have to expect that the Planetary Equipment items that are required in Citadels are also moving upwards at the speed of light also - though it is easier for supply to react given these items can be produced when players are doing other things or indeed when offline.

Now, i suppose the question is whether these items are going to remain at a high level (i.e. Citadels will be built then destroyed and so built again as an ongoing cycle) or whether they fall back to prior levels.

Either way, for those players that like to salvage - there is a good market for some items at present!

Broken Drone Transceivers have gone up 5x over the year.

Conductive Polymer has moved upwards about 3x.

Contaminated Lorentz Fluid has move up about 9 to 10x recently.

Contaminated Nanite Compound has moved up about 2 to 3x recently.

Scorced Telemetry Processor has move up about 15x.

Tangled Power Conduit are up 10 - 12x.

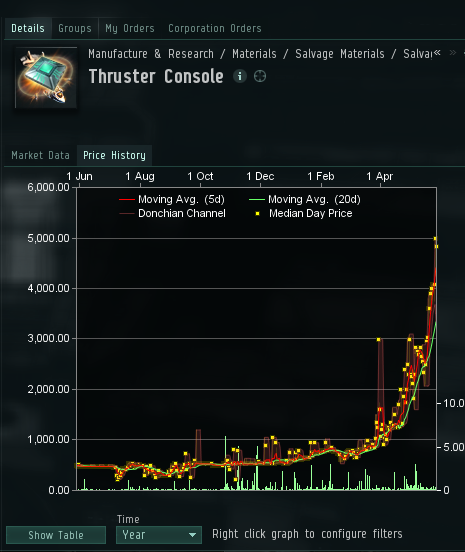

Thruster Consoles are up about 9x.