As at the end of April 2023 my wealth is 1 trillion ISK after paying 8.2bn to upgrade to Omega for another 30 days for four accounts. My Wealth increased by 65bn in April.

Technically, my wealth is 1.209 trillion ISK but i always take a 20% provision against Sell Orders to be conservative. Hence i quote 1 trillion.

Another pleasing month into what is normally a slower month after winter. I suspect i am benefitting from nothing more complicated that i have more items on the market to sell.

In April 2022 i had 412 bn of items for sale, today i have 1.2 trillion. In April 2022 my wealth increased by around 30bn, this April it rose by 65bn . . . . so makes sense. Wealth gets more wealth.

Target 1 trillion wealth achieved

There we go, i trillion of wealth in the bag.

what to do now? the obvious answer of 2 trillion could become quite tedious. My wealth increased by 632bn in the last 12 months. So making my next trillion i suspect would take 12-18 months.

But, when i set out this time back in August 2020 i wanted to experience more of the Eve ISK making avenues.

I do a bit of manufacturing on the side - i want to do a lot more of that.

Tried Planetary Interaction - it worked but was tedious and took too long.

Tried Invention - will give it another go.

So, lets see what i come up with.

Quick Summary

I definitely feel that the market is slowing down as we amble into the slow summer months.

The 65bn increase in wealth may say otherwise.

Currently, i can go some days during the week with very few sales. It all kicks off Friday to Sunday.

In fact, in the last few weeks it has not been uncommon for me to not log in some days because so few sales have been made.

That said, my Dodixie operation has attracted some additional competition that will need to be crushed. It is really important that competition is taken head on - if a new entrant feels that i am a sleepy operator they will gain in confidence. I need to extinguish their confidence before it gathers momentum.

Overall sales were down 14% to 315bn though this was 140% higher vs April 2022.

Sales fell in all my Omega Trading Hubs except Dodixie and Alentene. Dodixie was strong - recording sales of over 100bn isk.

My new Omega account that covers Arnon and Alentene this month failed to generate sufficient profits to cover the cost of the Plex to Omega the Account. This will be a focus for May. I need to get more items into those Hubs to make it work.

In the last 12 months i have made sales of 3.8 trillion isk and profits (after everything including Plex) of 632bn isk having spent 76bn on Plex.

The overall aim of what i do is to increase my wealth by at least 10bn per month. So far i have beaten that in 25 / 32 months i have been running this venture and indeed in all of the last 21 months.

A year or so ago the dream was to be making more than 1 billion profits a day including Plex costs to Omega the accounts. That has been achieved for each of the last 10 months. Lets see if i can go 2 more months.

For the last 6 months, my daily profits have been around 2.2 billion isk.

Activity

I continue to come on once a day to update Sell orders and replace items sold. About 30-45 minutes. Getting closer to 45 minutes these days.

I am experimenting with Manufacturing (ramping up slowly).

I stopped the Planetary Interaction - it was actually doing well enough to Omega an account but needed plenty of support and took too much time.

Over 99% of my sales and profits still come from Regional Trading.

Target 1bn profits per day after all taxes and plex costs

I have now achieved this aim for the last ten months. Was not expecting to but now i do expect to achieve this going forwards. The real test will be in the coming slower months.

In fact, over the last five months i have made over 2bn isk per day - that will be tricky to maintain over summer.

The big dream has to be making 100bn in a month.

Target daily sales required to achieve 1bn profits per day

In summary, i generally need to make 7.5bn sales per day assuming my item margin is 25%

As the cost of plex rises then my daily sales requirement also rises.

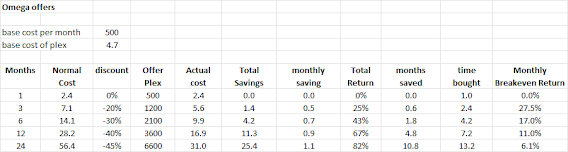

On the current taxation levels to make 30bn ISK per month i would need to cover:

- Plex costs of 3 x 500 x 4.7m = 7.1bn

- Courier costs 2% of sales (i.e. = purchase cost + collateral)

- Broker Listing fees 1.5% of sales

- Broker re-listing fees 0.3% of sales (lets assume all sales changed at least five times per month)

- Transaction Taxes 3.6% of sales

That all works out at 225bn monthly sales will generate profits after all costs including Plex of 30bn isk. = 7.5bn daily sales.

Bottom line is that assuming i make my 25% profit margins then each 1bn of sales creates profits of 164m and these go towards buying Plex for the Omega accounts and whatever is left is reinvested in the business.

Looking at some sensitivity analysis

- if my item margins were 28% instead of 25% then i need only make 192bn isk of sales (or 6.4bn per day)

- if Plex rose from 4.7m to 5.0m then then i need to make 228bn isk of sales (or 7.6bn per day)

1) Plex the four omega accounts - aim number one all the time - achieved

2) Hold sales in Dodixie to down 20% - achieved, was up 49%

3) Hold sales in Amarr to down 20% - missed, was down 34%

4) Hold sales in Rens to down 20% - missed, was down 33%

5) Hold sales in Hek to down 20% - achieved, was down 17%

6) Hold sales in Sobaseki to down 42% - achieved, was down 37%

7) Hold sales in Tush-Murkon Prime to down 20% - achieved, was down 7%

8) Ramp up Arnon and Alentene - achieved

9) Hold the investment and profits in Manufacturing - missed

So, on paper mixed but the positives were much stronger than the negatives.

Started a fourth Omega Account in January

I bit the bullet and started a fourth Omega account in January with trading Alts in Arnon and Alentene. Very early days and i was not really sure about it. So far, so good.

I am stocking up each alt by effectively reinvesting the profits from my business into these locations.

As expected, there is next to no competition much like Tash-Murkon and Sobaseki. So the sales may be low but the time requirement is very low. On some days, if i don't make any sales at one of these locations then i don't bother checking the prices - i know that there will be no competition. This is as close to "passive income" i think i will get.

Reminder of my Current Business.

For now 99% of what i do is inter-regional trading - buying from Sell Orders in Jita to sell elsewhere. The rest is made up from Manufacturing.

For Trading i focus on slow moving but high margin items. That keeps me away from fierce competition and i only need to sell an item once every 10 days to make good income. In other words, i don't really care if an item sells once every 10 or 20 days, if have many hundreds of items for sales across Eve and so each days a few items will sell and that generates all my income.

To put this in perspective. I had Sell Orders of 997bn up at the start of April which generate sales of 314bn. In other words, i sold between 1% to 2% of everything i had for sale every day. The is slow and i like it. Not for me the cut and thrust of high volume low margin world. Slow and easy for me. Tortoise and hare stuff.

For this side of my business, lets call it Merchanting or inter-regional trading, i want to generate profits of 10bn ISK per month after paying to Plex my account. Given i now have eight Omega alts in Amarr, Dodixie, Rens, Hek, Sobaseki, Tash-Murkon Arnon and Alentene i am hoping that this 10bn aim will be easily achieved.

My business model evolves over time. As my wealth increases i focus on higher value items. Therefore, i try also to stick to the rule of making a minimum of 100m profit per item sold. i.e. if i buy an item for 70m then i aim to sell it for at least 170m isk. This makes sure i don't waste my time on making low absolute profits and so preserves the 45 minute rule.

My main business is operated with four omega accounts (paid for with plex) with twelve alts.

The main Trading alts sit in Dodixie, Amarr, Rens and Hek. I have also omega alts in the new Trading locations of Sobaseki (in Lonetrek), Tash-Murkon Prime (in Tash-Murkon), Arnon (in Essence) and Alentene (in Verge Vendor).

The other four alts sit in Jita and buys from Sell Orders, has these items couriered to the alts in Dodixie / Amarr and Rens / Hek and Sobaseki / Tash-Murkon Pime and Arnon / Alentene who then put them onto these markets for sale.

The Jita alts also serve to sell items that i can no longer sell in my trading locations Sort of clearance sales.

I also started in December 2021 to place alpha alts in other regions to see how it goes. I just need two of them to demonstrate that they can combine to justify an Omega account. Also, they need to take up very little of my time. So far the Sobesaki / Tash-Murkon alts and Arnon / Alentene made the grade and were upgraded in two accounts.

The other regions so far are: Placid; Citadel and Khanid. And i am in an NPC station in Delve and Outer Ring. I have started in Venal.

I am struggling to make the Low Sec locations work.

Jita

Traditionally i never sold anything in Jita unless it was being transported back from one of my trading hubs because i could not sell it and so to be sold at Jita prices to get some isk back.

Then in September 2022 whoever was selling ship Blueprints in Jita fell asleep at the wheel and i moved in. In November Jita was my top selling location.

But all good things must come to an end and competition returned by February.

So from sales peaking at 103bn in November 2022, in April sales in Jita were a mere 22bn which is more than double the pre-September 2022 era but remains in a declining trend.

I also do station trading in Jita (that is - put Buy Orders up in Jita and then when those Buy Orders are executed i then put the item up for Sale in Jita at a higher price). I stick to the slow moving items again. That said, i don't actually know how much this earns me.

Manufacturing

I am now nine months into my Manufacturing project. It remains slow and i need to up my game (i know, i said that before).

In Aprili made 7bn of sales generating an item profit of 0.9bn and so after taxes a profit of 0.8bn.

Not good at all. Again.

When i get time, i really need to look deeper into this and get things ramped up.

Other High Sec Trading Locations

I don't want to spend all my time on Eve doing Regional Trading (buying from one region, mainly Jita, to sell to another) but i do want to see if i can find really low competition but stable revenue streams of trading.

The current alpha account regions so far are: Placid; Citadel and Khanid. And i am in an NPC station in Delve, Outer Ring and now Venal.

My alts in Arnon and Alentene were upgraded to Omega during January.

The alpha trading locations made combined sales of 1.6bn in April vs 1.2bn in March. I have been scaling back. I don't replace the sales made anymore.

The trial has been done, i feel i know what Locations are best and which don't work.

Delve

I want to experiment with selling in null/low Sec. Hence, i have found an NPC station in Delve and started experimenting with items to sell.

It is not going well - sometimes threatens to improve but then fall back again.

As with my other alpha accounts i am letting it wither away on the vine.

I am rethinking how to make low/null sec work.

Plex

I am aim to store up to 6 months of Omega for each of the Omega accounts which would mean buying 12000 Plex (= 6 x 4 x 500).

I now have 4500 in stock - so no change during March. I don't plan on buying any Plex in the near term given my surplus isk is going into stocking up on the Arnon and Alentene trading locations.

That said, CCP are changing their attitude to Omega prices and there is a permanent sale on that gives a discount to the Plex required for longer periods of Omega purchases.

A minor accounting point (again)

Similar to back in September 2022, i have to think how i account for buying three months of Omega for each Omega account (4 accounts). I repeated this in December and again in February.

Hence, in the December deal and in February i spent 26bn and 18bn respectively buying 3 month Omega deals for Plex.

The way i account for this is to hold the entire amount as wealth and reduce this "asset" by a month at a time.

The alternative accounting treatment would be to count the 26bn and 18bn as costs in the month they were expensed which means December and February would look week but January, March and April stronger.

It all adds up to the same number just the timing of recognising the cost is different.

Analysis of Trading Profits

In total i made 315bn ISK of sales in April which made me item profits of 105bn ISK.

(item profit is the simply difference between sales done vs costs spent buying products, so before fees and taxes. Because i don't yet invest in items other than Plex i don't make any allowance for items still in stock - in part because i don't track the cost per item spent).

Overall, sales fell by 14% in April which was all Trade Hubs down except Dodixie and Alentene.

Dodixie was the best selling Trade Hub at over 100bn followed by Amarr at 70bn. Rens was 38bn and Hek 32bn. Sobaseki + Tash murkon did 26bn whilst Arnon + Alentene did 11bn.

The item profits of 108bn was an item margin of 33.2% (105/315) vs my target of 25%. This is another good month for margins.

From this I then need to take a whole series of costs off before i get to my Business profits (and notice how they are more related to Sales rather than costs):

Courier Fees: i aim to pay 2% of sales value to the Courier = 8.1bn

Sales tax cost me 11.6bn ISk (=3.69% of sales) - the Dodixie, Amarr, Rens, Hek Sobaseki, Tash-Murkon and Jita characters are level 5 in Accounting (=sales tax of 3.6%); Alentene and Arnon are training up, and of course all the alpha alt accounts are only Level 1 (=sales tax of 8%).

Broker Fees costs me 11.5bn (=3.7% of sales, Dodixie is more competitive so i was changing prices more). Now, i can break this down into the initial listing fee of 1.5% (because i am Level 5 Broker Relations on all Omega characters and lets to make the sums easier and include all the alpha alts) and therefore the rest is the cost of changing the price which is 0.30% a shot (i may have that 0.30% completely wrong!).

So, Listing Fee = 1.5% x 315= 4.7bn and so the Relisting Fee = 11.5-4.7 = 6.8bn which is 2.2% of sales. That shows that i do change prices quite often, bias to Amarr, Jita and now Dodixie. Someone is taking me on in Dodixie. Will need to be crushed.

This takes my 'Business Profits' to 73bn ISK for April vs 76bn in March. This is what 30-40 minutes a day in April gave me.

So, the post-tax margin is 23.1% (73/315) and so i achieved the 15% target.

The omega charge was then 8.2bn (see above in Plex section)

That, therefore, is the road map from 315bn sales to 65bn increase in wealth.

Items i am selling in Dodixie, Amarr, Rens, Hek, Sobaseki, Tash-Murkon, Arnon and Alentene

No Change all year really.

I sell blueprints, skill books, implants and ship equipment.

I am trialling selling structures like jump gates.

Blueprints i think have stabilised. I have all but been kicked out of selling blueprints in Jita. Too competitive.

Implants are doing well and tend to be the most competitive - i am slowly expanding into more types and moving up the ISK value curve. And rolling them out to all my Trade Hubs. I now keep to implants costing over 100m ISK and up to 2bn ISK. They don't sell well but when they do i tend to get a whole family sold at a time. Again, that's how i like it. A billion or so of investment can take 30 days to sell. I am seeing more instances of whole family's of implants being sold at once.

Mining equipment also feels like it has stabilissed at a low level - feels like there are players coming back who need mining equipment.

Skill books are now my lowest income generator - very few sales now. Barely happening at all.

Ship Equipment is doing well. I think has been gathering momentum all year.

Rigidly sticking to the 25% margin target. Courier fees and taxes now take 9% of that to bring me to a theoretical 16%.

Courier Contracts

Each night, i get home from work and determine what i need to sell in all the locations.

The time is taken changing prices were necessary (especially Amarr given it is competitive and increasingly Dodixie) and then figuring out what to sell with the ISK made from the prior 24 hours sales.

I have a list of items that feature regularly and i add to this list as time goes by. So is a case of checking Jita prices vs current location prices.

It takes a minute to check all the alt accounts.

To look up prices in Eve I am using Eve Tycoon which seems to have more of the latest items in its market browser. I used to use evemarketer but i just got used to Eve Tycoon.

Each night i courier about 5 to 15bn ISK of items from Jita. Used to be 2-10bn but things are better these days and i have more items up for sale. The total cargo volume is 10-250m3 per shipment. So small but valuable items. But this allows the couriers to use small, fast ships with much less chance of being ganked. So there is always someone willing to pick up the contract quickly.

I pay a generous 1.5 to 2.0% of collateral as fees. I am more interested in getting my items onto the market quickly than penny pinching on distribution costs.

Outlook

May will have ten very conservative aims - I expect May will be slow, i can feel it already. Hence, the aims will be:

1) Plex the four omega accounts - aim number one all the time

2) Hold sales in Dodixie to down 20%

3) Hold sales in Amarr to down 20%

4) Hold sales in Rens to down 20%

5) Hold sales in Hek to down 20%

6) Hold sales in Sobaseki to down 20%

7) Hold sales in Tush-Murkon Prime to down 20%

8) Ramp up Arnon and Alentene

9) Hold the investment and profits in Manufacturing

The daily sales in April averaged 10.5bn.

Current wealth is 1 trillion ISK made up from:

- Plex held as an investment 22bn ISK

- Items in hanger for sale 5bn ISK

- Items in hanger for use in business 11bn ISK

- Omega brought forward 18bn ISK

- Buy orders on the market 42bn ISK

- items for sale 1043bn ISK

- less a 20% provision 209bn ISK*

When i add up my wealth, I don't count assets I use in the course of my business such as ships, fittings etc nor do I add back any expenses such as skills purchased etc. The wealth I disclose is made up of items that are ISK or are in the process of being converted to ISK or are used to generate isk that can be readily resold back onto the market. Any ships or skills or fittings etc i buy are counted as expenses in that month. The only exception to this rule is Blueprint Originals i use for manufacturing. They are held at cost.

* I take a 20% provision against the items I am selling. Eve calculates wealth by adding up the value of the sell orders hence it is possible to increase your wealth by buying an item for 100m ISK and putting a sell order for 120m ISK (in this case your wealth would increase by 20m ISK). For me, I want my wealth to be calculated at cost. I know that the value of my sell orders will likely fall over time as I update my orders downwards as competition reduces their prices before my items are sold. Hence the 20% provision is my best guess as to what the maximum reduction I would need to make to my sell orders as a whole before they are sold. In an ideal world I would value my sell orders at the value which I bought the items for.